Medicare

What is Medicare? Medicare is health insurance for people 65 or older. You may be eligible to get Medicare earlier if you have a disability, End-Stage Renal Disease (ESRD), or ALS (also called Lou Gehrig’s disease).

Let’s go over the history of Medicare, the basics of what Medicare is, what it covers, who is eligible, and when they should enroll. We’ll cover what Medicare costs as well how people fill in the gaps in Medicare. And we’ll examine Medicare Supplement plans (Medigap), Medicare Advantage plans, and Part D prescription drug plans.

Also, what you'll need to know if you plan on working past 65.

For OEP (Open Enrollment Period or AEP (Annual Enrollment Period) - to research plans, make an appointment or to sign up, go to the Medicare Open Enrollment page

History of Medicare

Medicare Parts

When to enroll

Medicare costs

Medigap / Medicare Supplement

Medicare Advantage Plans

Working beyond 65 years old

The beginning, the day Medicare began-

July 30, 1965: President Lyndon Baines Johnson signed Medicare into law

Former President Harry Truman was the first recipient. He and his wife Bess received cards 1 and 2

19 million beneficiaries were initially enrolled

A, B, C, D ?

We’re talking about Medicare, not the alphabet - It’s all about “the parts”

Part A = Hospital Coverage

Medicare Part A- What does it cover?

Inpatient hospital stay- semi-private room, three meals a day

Inpatient meds - Drugs administered as part of a hospital stay

Skilled Nursing Care (up to 100 days) - Covers care of up to 100 days in a Skilled nursing facility after a qualifying three-day hospital stay – DOES NOT cover long term care!

Blood transfusions

Hospice

Part B= Outpatient Coverage

Medicare Part B- What does it cover?

Doctor visits

Lab work

Preventative care

Outpatient surgeries

Physical therapy

Diagnostic imaging

Dialysis

Chemotherapy

Part B drugs

Part B covers 100% of preventive care, and 80% of all other outpatient care

While some preventive care (i.e. flu shots, yearly wellness exams, mammograms, etc.) are covered at 100%, Part B covers most other outpatient services at 80%.

Original Medicare

Under Original Medicare, you get your benefits directly from the federal government

Part A + Part B= Original Medicare

Back in the 1960s, Blue Cross plans were popular, providing hospital care and outpatient care. Medicare was modelled after these plans and that’s why it has the two parts we just covered; Part A for hospital care and Part B for outpatient care. These two parts are often referred to as Original Medicare or Traditional Medicare, and these are the only two parts where you get your benefits directly from the federal government.

Medicare Part C and D came later and are provided by private insurance companies

Part C: Medicare Advantage

Private insurance plans that pay instead of Medicare.

Part A + Part B + Part D = Part C, Medicare Advantage

Medicare Part C is also known as the Medicare Advantage program. It was signed into law by President Clinton as part of the Balanced Budget Act of 1997. It’s an optional way to get your Part A and B benefits through a private insurance company instead of from Medicare itself.

Part D: voluntary drug program

How it works

Pick your plan through a private insurance carrier in your area

Pick up your prescriptions from an in-network pharmacy

Shop your Part D plan each year during the fall open enrollment

Medicare Part D is the newest part of Medicare. It’s optional private insurance to help reduce the cost of your outpatient prescription drugs.

Although it is optional, if you do not sign up when you are first eligible and you do not have other creditable drug coverage, you will incur a penalty for not enrolling. The penalty is cumulative and gets larger with time.

Once you enroll with a private insurance carrier, you will receive a coverage card and be able to purchase your drugs at a reduced cost from in-network pharmacies.

It is recommended that you shop your Part D plan each year during the fall enrollment period to make sure you have the best coverage for you based on your current medication needs.

Enrolling in Original Medicare

You enroll for Parts A and B through Social Security or Railroad Retirement Board (RRB)

If you’re already receiving Social Security benefits: your enrollment is automatic

Most people sign up for Medicare online at socialsecurity.gov or in person at their local Social Security office. Railroad retirees sign up through the Railroad Retirement Board (RRB).

The only people who don’t need to actively enroll in Medicare are people who are taking SS income benefits prior to age 65. These people are auto-enrolled in Medicare Parts A and B at age 65. The card will just arrive in your mailbox about one to two months before you are eligible for Medicare at 65.

Initial enrollment period (IEP)

It is a 7-month window- It begins 3 months before and ends 3 months after your 65th birth month for a total of 7 months

For example: If you turn 65 on May 20, your Medicare IEP would run from February 1 to August 31.

Your Medicare start date depends on when you enroll

•Medicare start date is the first of the month after application date

Enroll prior to birthday month:

Enroll in or after your birthday month:

Medicare start 1st of the month of your 65th birthday

Unless you're born on the 1st

Your Medicare start date will depend on WHEN you enroll during your 7-month enrollment window. If you want benefits to begin on the 1st day of the month you turn 65, then you need to enroll in the 3 months before your birthday. If your birthday is on the first of the month, your coverage starts the first day of the prior month.

Example:

Mr. Smith’s 65th birthday is July 20. If he signs up for Medicare in April, May or June, his coverage will start on July 1.

Now assume Mr. Smith’s 65th birthday is July 1. If he signs up for Medicare in March, April or May, his coverage will start on June 1

If you enroll in your birthday month or the 3 months after your coverage will start the first of the month following the application date.

People who are still working for a large employer may enroll in just Part A at 65 and delay Parts B and D until later when they retire – more on this later in the presentation. Note that if you do enroll for Part A, you can no longer contribute to an HSA (Healthcare Savings Account)

Medicare Cost Sharing

How much is this all going to cost?

Some perspective…

Before applying for Medicare, If you’re insured through an employer-

You pay a premium, often through paycheck deduction

This is the cost of the insurance. It’s referred to as a monthly premium

You pay co-pays and/or co-insurance when you use medical services,and you likely have an annual deductible-

This is the cost-sharing

Just like with the insurance you may have had while you were under 65, Medicare has two types of costs that you will share in.

The first is the premium you pay for the coverage itself and the second is the cost-sharing you pay as you use health services.

Medicare’s costs –

Out-of-pocket expenses

Medicare Part A- Hospital

Part A costs nothing if you have worked and paid FICA taxes for at least 40 quarters (10 years.) Most people pay $0 for Part A because you paid FICA taxes during your working years.

You’re considered “paid up” so Part A will cost $0.

You can qualify for this free Part A under your own work history or a spouse’s work history if you have been married at least 1 year. Spouse must be eligible for SS benefits.

You can qualify under a divorced spouse’s work history if married at least 10 years and spouse is eligible for SS and you are single.

You can qualify if you are widowed and were married for a least 9 months before spouse died and you are single.

What happens if you don’t have enough work history? Well, in that case you can pay for Part A.

The costs:

If you have between 30–39 quarters of work history, you can buy Part A pro-rated at $311/month in 2026

If you have less than 30 quarters of work history, you can buy Part A at $565 in 2026

Medicare’s costs

Out-of-pocket expenses

Part B and Part D - YOU pay monthly premiums.

The Monthly Premiums:

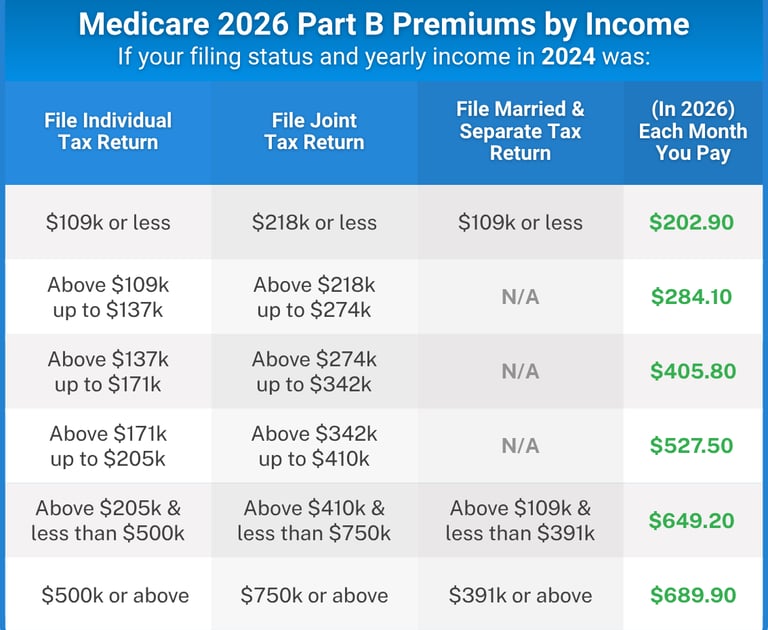

Part B- Monthly premium is $202.90/month in 2026 for new enrollees

•Deduction monthly from SS check, or billed quarterly if not taking SS yet

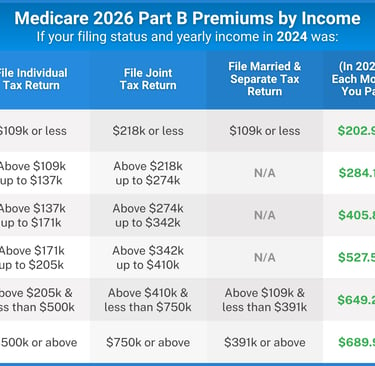

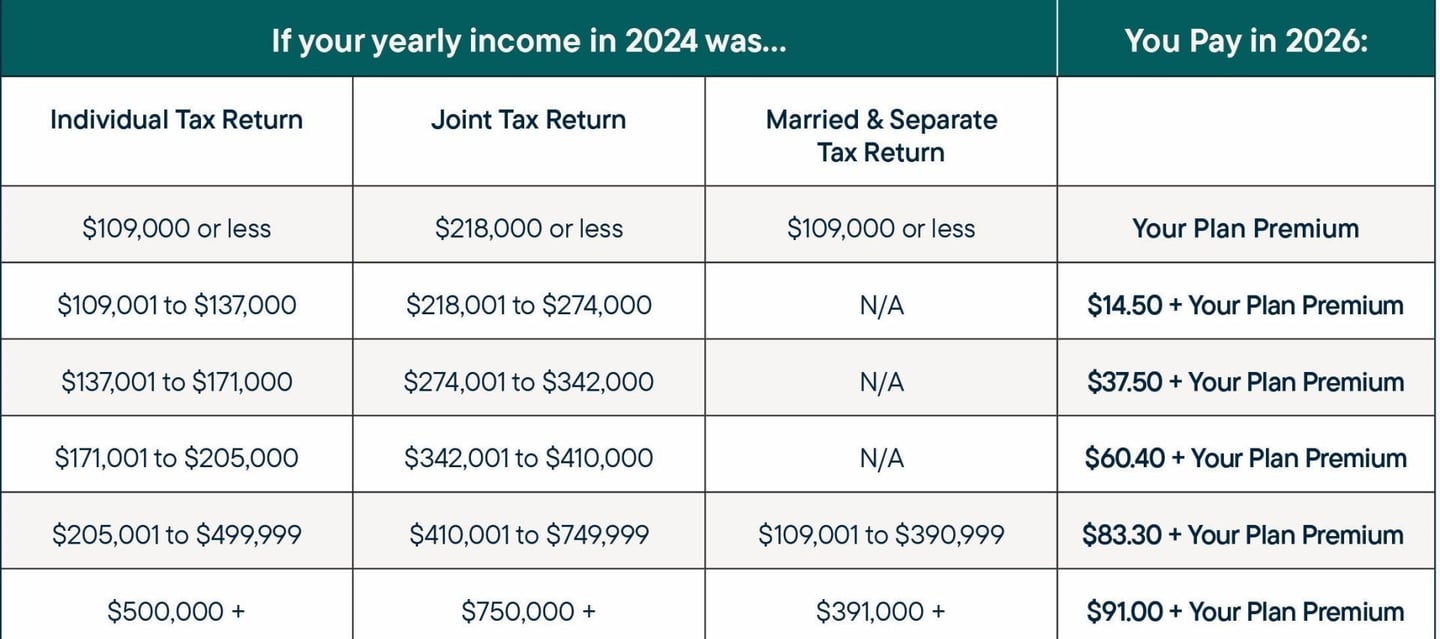

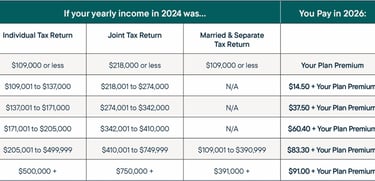

IRMAA for high-earners - Individuals earning more than $109K (individual) $218K (joint) have a sliding scale for Parts B and D based on modified, adjusted gross income on your tax returns

For Parts B and D you will pay monthly premiums.

Most Medicare beneficiaries pay the standard base Part B premium of $202.90/month in 2026

It is deducted monthly from your social security check or billed quarterly if not yet receiving social security benefits.

However, around 5% of beneficiaries pay more because of higher incomes. When you have higher income (over $109,000 if you are single, over $218,000 if you are married), you pay what is referred to as an Income-Related Monthly Adjustment Amount (IRMMA) on top of the base premium.

Monthly premiums for Part B new enrollees

Based on your 2024 modified adjusted gross household income, your 2026 Part B premium will be based on a 2-year lookback:

Social Security calculates your Part B premiums each year based on your tax return from two years prior.

The Social Security Administration mails you a letter each December to notify you of the new calculated Part B premiums for the upcoming year.

If your income was higher before due to working, but you have now retired and that income is lower, you can file an appeal with SS office indicating work stoppage, and request that the premiums be lowered. There is no guarantee of approval but it costs nothing to appeal.

To appeal:

Submit Form SSA-44, which can be found on the Social Security Administration (SSA) website

Select the life-changing event reason for appeal: work stoppage, work reduction, marriage, divorce, or death of a spouse, loss of a pension, loss of an income producing property or employer settlement payment that has affected your income

Part D premiums- What to expect

Part D drug plan premiums are set by the insurance company who is offering the specific Part D plan.

There is a wide range of premiums (from as low as $0/month to over $100/month), but if you averaged every beneficiary out there on a stand-alone Part D plan, you would find the national average Part D premium to be around $55.50.

Just as with Part B, if your income is higher, you will be assessed an Income-Related Monthly Adjustment Amount on top of your Part D premiums.

Medicare doesn’t offer Part D plans itself, but it does track whether you enroll in Part D and maintain coverage. If you don’t and you don’t have other creditable coverage, you are assessed a late penalty of 1% for every month that you waited to enroll and is paid each month–forever–once you do finally sign up.

Monthly premiums for Part D new enrollees

Based on your 2024 modified adjusted gross household income, your 2026 Part D premium will be (2-year lookback):

Medicare recalculates these rates annually based on your IRS tax returns.

If you appeal your Part B premiums because you have lower income now than you did two years ago, that appeal will also apply to any Part D and Income-Related Monthly Adjustment Amount (IRMAA) that is assessed. In other words, only one appeal needs to be filed.

Part A Cost-sharing - 2026

Part A deductible: $1,736 (for each benefit period)

$434 Daily copay on Day 61

$868 Daily copay on Day 91

ALL COSTS after Day 150

First 3 pints of blood

$217/day coinsurance for days 21–100 in skilled nursing

Whenever you seek healthcare services, Medicare will pay a portion of the costs and you’ll pay a portion.

A daily copay of $434 starting on Day 61 to day 90. After day 90 the co-pay goes up to $868/day for what are called lifetime reserve days. Each person has only 60 of those over their lifetime. After day 150, you pay all costs.

You will also pay for the first three pints of blood if the hospital has to pay for blood instead of getting from a blood bank

A Medigap plan will help to cover these and will also provide you an extra 365 days in the hospital beyond day 150.

Part B Cost-sharing - 2026

Part B deductible: $283

Medicare pays 80%, you pay the other 20% coinsurance

No cap – you pay 20% forever

On the Part B side, you owe:

A calendar year deductible

Then Medicare pays 80% you pay 20%.

Here’s the very important part to consider when making your decision on coverage… There is no cap or out of pocket limit – you pay the 20% co-pay on everything.

There are options to limit these costs existing in the form of Medigap or Medicare Advantage plans

Private Market Plan options

= Higher premiums, less cost-sharing

=Lower premiums, higher cost-sharing

There are two routes you can go to cover the gaps with Medicare: a Medicare Supplement plan (also called a Medigap Insurance Plan) or a Medicare Advantage plan. You can only have one or the other, not both.

Generally speaking, a Medicare Supplement has higher premiums and less cost sharing whereas a Medicare Advantage plan has lower premiums and higher cost sharing. Both are offered through private insurers.

Medicare Supplements Plans (Medigap)

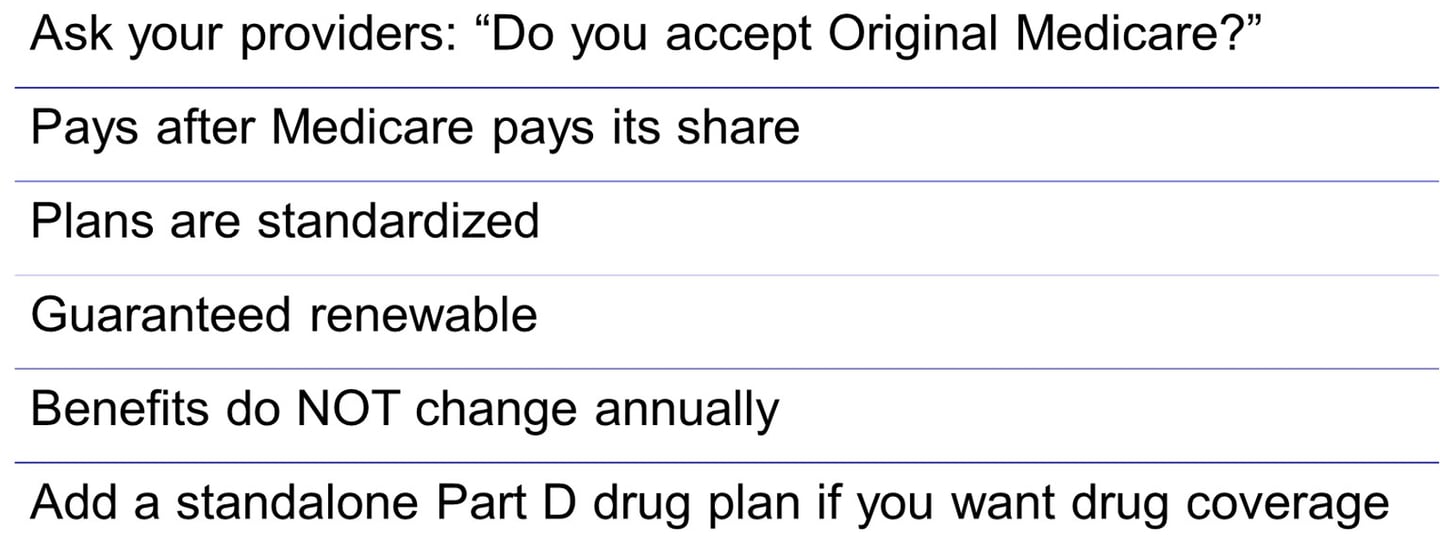

Medigap plans have been around since the 1960s and these private policies pay after Medicare first pays its share of your bills. Medigap plans allow you to see any doctor that accepts Medicare. You don’t have to choose a primary care provider (PCP) or get a referral in order to see a specialist. You can see any of the over 1M providers who accept Medicare and it doesn’t matter which insurance company you buy your Medigap plan from.

This works well for people who travel a lot in the United States as they can see doctors in any state.

Medigap plans were standardized in 1990 to make them easy for consumers to compare. They’re offered by many different insurance companies.

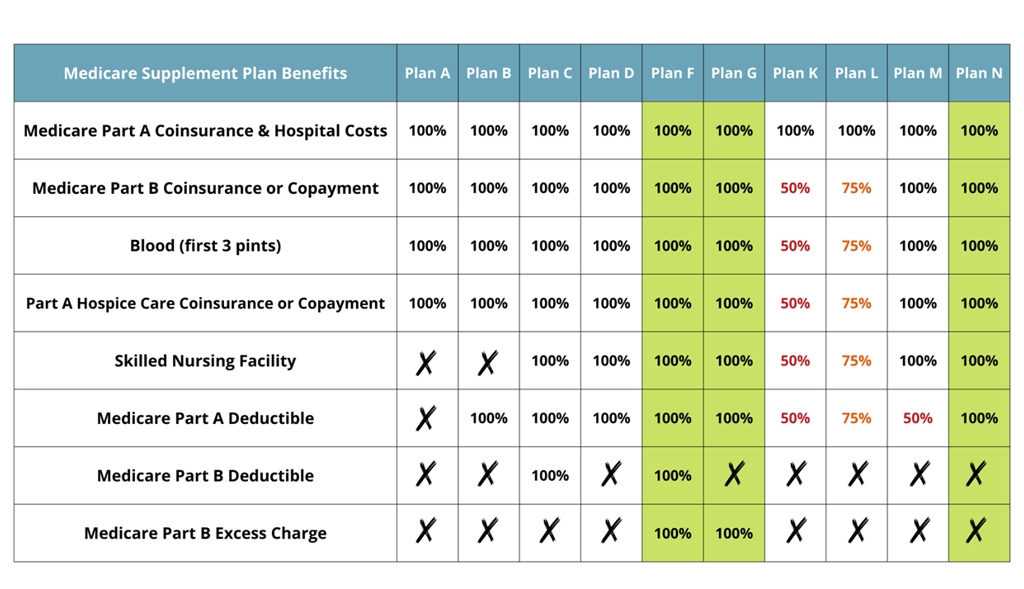

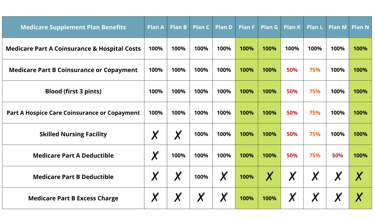

Medicare Supplements (Medigap)

Coverage by plan

Currently there are 10 standardized Medigap plans, each one covering a different set of benefits. The two most popular plans are Plan G and Plan N. You can choose a very comprehensive plan like Plan G that covers everything except for the Part B deductible. Or you can choose a plan with lesser coverage because you agree to do some cost-sharing. Plan N is an example where you can get lower premiums than Plan G but you agree to pay doctor copays and E.R. copays and any excess charges you might incur from non-participating providers.

Plan F is the most robust plan on the chart, and it covers all of the gaps in Medicare Part A and B.

However, only people who were eligible for Medicare prior to January 1 of 2020 can get Plan F. This is because Congress passed legislation that outlaws Medigap plans that cover the Part B deductible. It wants everyone to have to incur a deductible so that people think twice before running to the doctor for minor things

Medigap monthly premiums

What to expect

Monthly rates vary based on age, zip code, gender, tobacco use, and eligibility for household discounts.

Rates are lowest in IA, IN, OK, MS, NM

Rates are highest in FL, CT, WA, ME and NY

Medigap companies set their own rates. Insurance agents/brokers can’t change them.

Medigap companies base their rates on several factors. The rate is the rate–a broker cannot change that, so whether you call an insurance company directly or you call a broker who works with multiple companies; both will quote you exactly the same rate for a policy based on things like age, zip code, gender, tobacco use, and eligibility for household discounts

Medigap premiums are in addition to what you pay for Medicare itself, so you would add the Part A, B, and D premiums together plus the Medigap premium to get your total monthly expenditure. Plans vary widely in price based on region and the costs of healthcare in that region. For example, someone in Florida might pay twice the premium that someone in Texas pays.

Brokers can quote all the companies in your area to see who is offering the lowest price for the plan you want.

Qualifying for Medigap

Your eligibility for enrolling in a plan varies

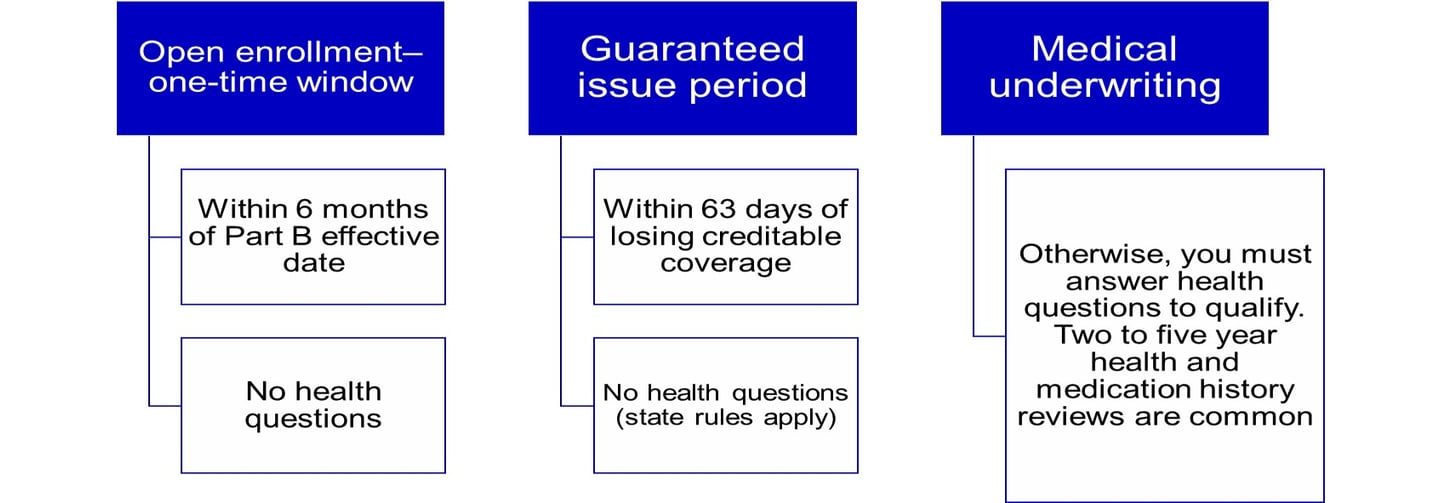

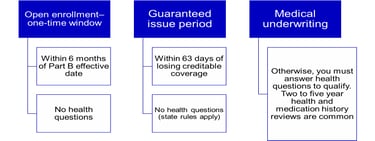

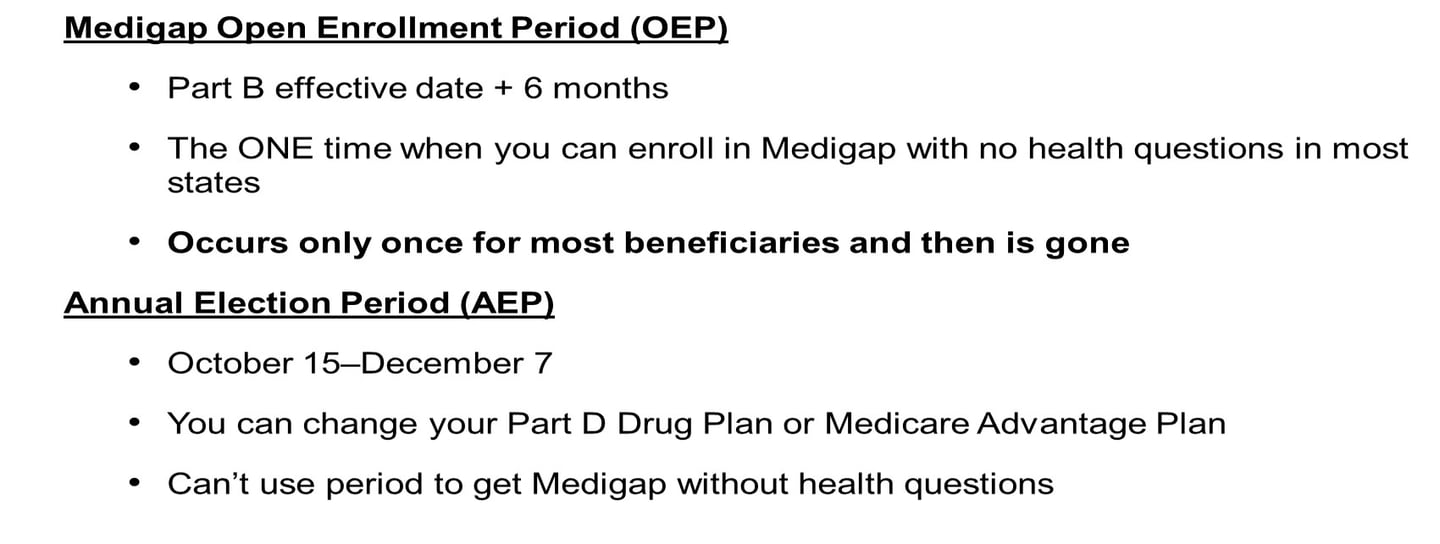

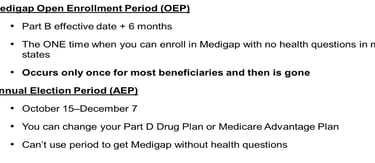

Beneficiaries new to Medicare have a limited, one-time, six-month open enrollment window to get any Medigap plan they want, with no health questions asked. Coverage is guaranteed when you enroll during this window.

That window starts with your Part B effective date and ends six months later. Applying after that point will require health questions and the carrier can turn you down for preexisting health conditions.

There is also a more limited window called a guaranteed issue period (depending on the state you live in). This applies in special situations, such as when someone is already enrolled In Parts A and B and is losing employer health coverage that coordinates with Medicare. These people will have a shorter, guaranteed issue window to apply for certain Medigap plans with no health questions asked. State rules may apply.

States with exceptions

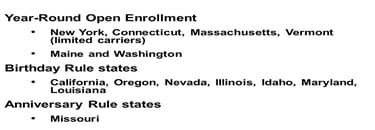

Some states have adopted more lenient rules. Here are some examples:

While beneficiaries in most states will get just the one, six-month Medigap open enrollment window, there are expanded rules in some states. For example, people in New York have year-round open enrollment. People in California can change during a limited period of time surrounding their birthday each year if they have an existing Medigap plan and want to switch to a cheaper plan with equal or lesser benefits.

Where many people go wrong is that they assume that they can sign up for a Medigap plan during the fall annual election period without health questions and be guaranteed coverage.

This isn’t necessarily correct. The fall Annual Enrollment Period (AEP) is for changing your Part D drug plan or Part C Advantage plan. It doesn’t have anything to do with Medigap plans and does not give you a free pass into a Medigap plan.

Once you have a Medigap plan, you can switch plans or carriers but you have to apply (health questions). If your application is accepted you have a 30 day free look period to decide if you want to keep it. You will have to pay both premiums that month.

What are the common reasons people switch Medigap policies?

You’re paying for benefits you don’t need

You need more benefits

You want to change your insurance company

You want a policy that costs less

What can go wrong?

Disadvantages of Not Getting a Supplemental Policy

What if I decide to do nothing?

High Out-of-Pocket Costs: This is the most significant risk. Without a supplemental policy, you are responsible for all of the out-of-pocket costs that Original Medicare doesn't cover. This includes the Part A and Part B deductibles, as well as the 20% coinsurance for Part B services. A major medical event, like a hospital stay or a serious illness requiring extensive treatments, could result in thousands of dollars in medical bills.

No Yearly Limit on Out-of-Pocket Spending: Unlike many Medicare Advantage plans, Original Medicare has no annual limit on what you have to pay out-of-pocket. This means that if you have a catastrophic medical event, your costs could be unlimited, which can be financially devastating.

Limited Coverage for Travel: Original Medicare generally doesn't cover care received outside the United States. Many supplemental policies, however, offer some coverage for foreign travel emergencies.

Difficult to Enroll Later: Your initial Medigap Open Enrollment Period starts the month you turn 65 and enroll in Medicare Part B. During this 6-month period, insurance companies cannot deny you a policy or charge you more due to pre-existing health conditions. If you miss this window and decide to get a supplemental policy later, you may be subject to medical underwriting. This means an insurer can deny you coverage (depending on what state you reside in) or charge you higher premiums based on your health history.

Medigap Summary

Recapping what you need to know

Medigap plans give you freedom of access to see any provider nationwide accepting Medicare. The only question to ask the doctor is: Do you take Medicare? If the answer is yes, then you can use any Medigap plan there and it will cover you just as it is supposed to. Medicare processes your claims and then pays its share and sends the remainder of the bills on to your Medigap plan to pay their share. Plans are standardized by the federal government to make them easier to compare, and they are guaranteed renewable, which means they can’t drop you for getting sick. Another great thing about Medigap plans is that their core benefits do NOT change from year to year like Medicare Advantage plans do.

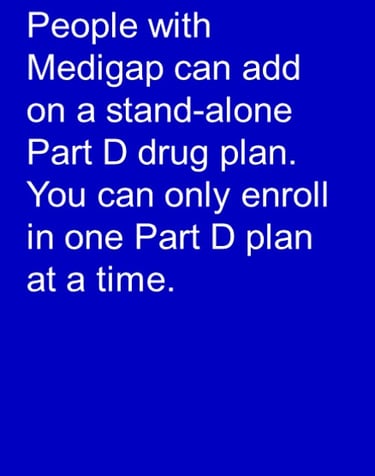

Lastly, Medigap plans only supplement Part A and B Benefits. They do not provide outpatient drug coverage so you would need to add a standalone Part D plan for that.

Stand-alone Part D

You’re eligible to enroll in a Part D drug plan during your Initial Enrollment Period to go alongside your Original Medicare and a Medigap plan.

If you miss your IEP, then you can enroll in a Part D plan during the Annual Election Period each year in the fall but you will pay a penalty.

You must be enrolled in Part A and/or B to eligible.

You must also live in the plan’s service area to be eligible to enroll in that plan.

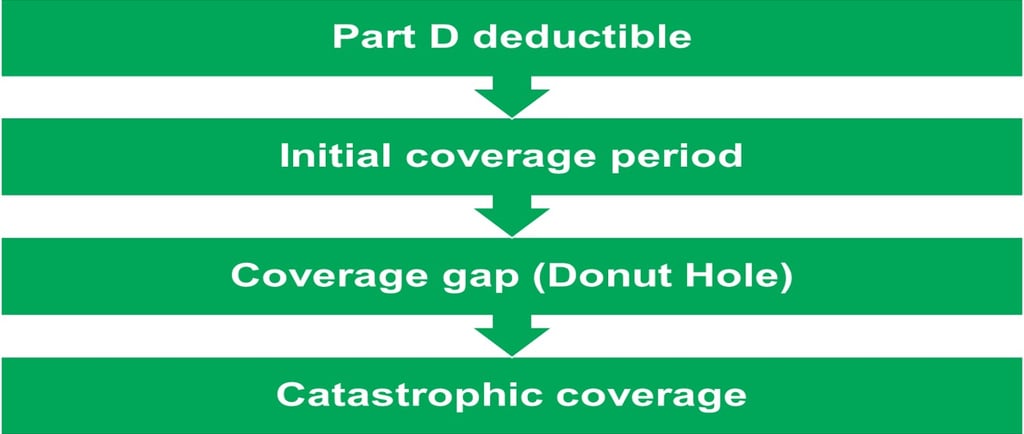

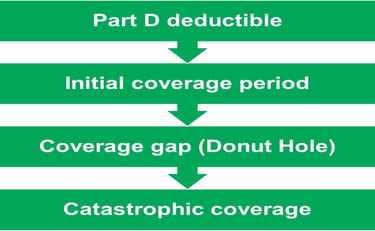

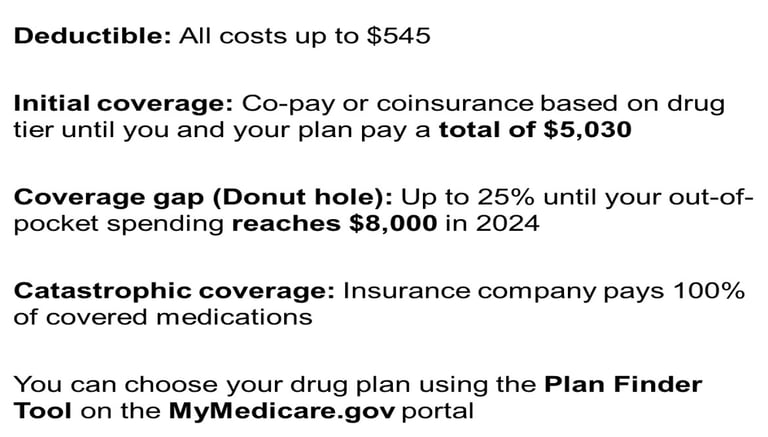

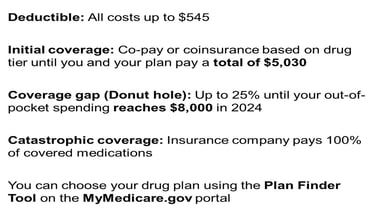

Part D has four stages

Medicare sets the limits for each of these stages every year

Part D drug coverage is more complicated than what people are used to with employer coverage. Medicare itself sets the minimum required guidelines for Part D and all Part D plans have the same basic structure with 4 stages. For example, in 2025, the maximum deductible that a Part D plan can build into their coverage is a $590 deductible. The plan can require this whole deductible or it could offer their plan with a lesser deductible or it could waive the deductible altogether. Most plans use the full deductible. Many Medicare beneficiaries are unused to a deductible on outpatient drugs, so sometimes this comes as a surprise that they have to pay out of pocket for medications until that deductible is satisfied

The most important part of any drug plan is the catastrophic coverage, where as of 2025, the insurance company pays 100% of covered medications

Medication costs

What you pay for medications will depend on which stage of the drug plan you are in and which tier a medication falls in:

After the deductible, Part D plans will pay most of the cost of your medications, with you just paying a copay or coinsurance for each medication depending on which tier it falls into.

Most Part D drug plans use 5 tiers. The insurer can assign a drug into any tier based on the retail cost, but what you see most often is:

Tier 1: Preferred generics

Tier 2: Non-preferred generics

Tier 3: Preferred brands

Tier 4: Non-preferred brands

Tier 5: Specialty meds

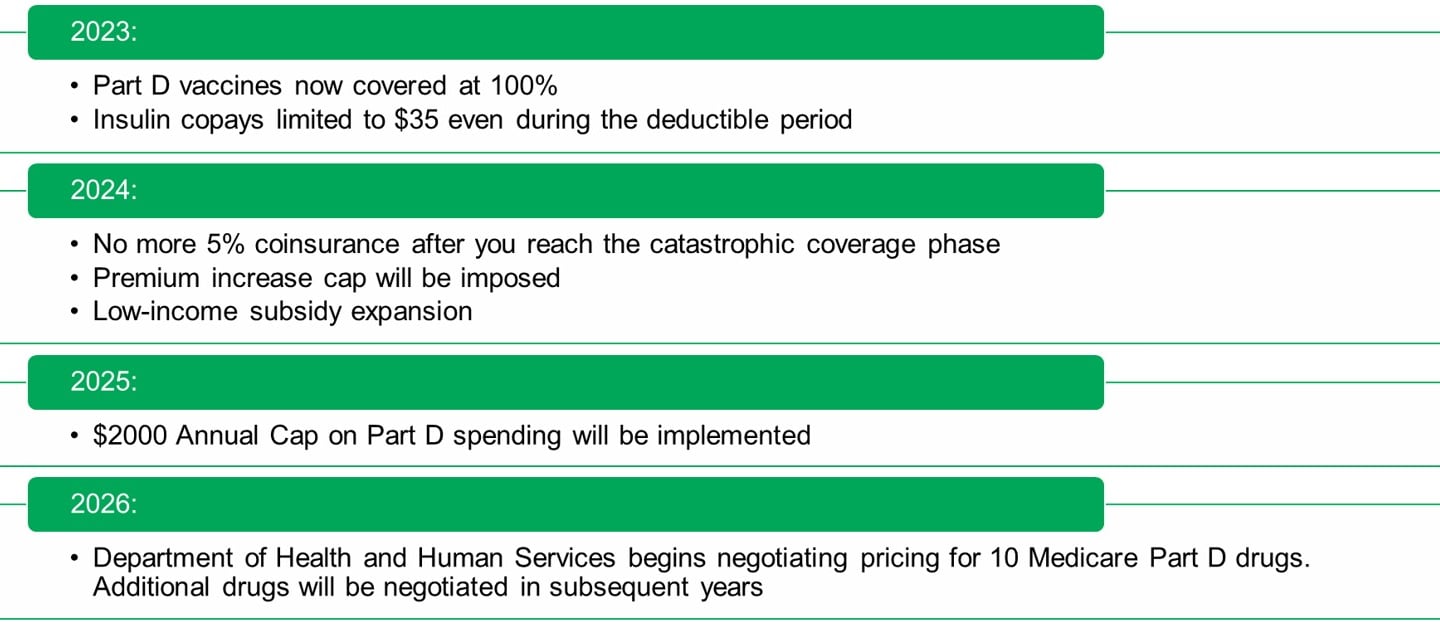

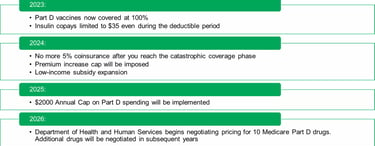

Inflation Reduction Act of 2022

Positive changes to Medicare Part D

Changes beneficiaries will see in 2025:

Beneficiaries will not spend more than $2,000/year on out-of-pocket costs related to Part D.

Changes beneficiaries will see in 2026:

Certain high-priced and single-sourced drugs will now have negotiable prices meaning more affordable access to drugs for seniors.

Medicare Advantage Plans

How do they work?

About 90% of Medicare Advantage plans also include a built-in Part D Drug plan.

You must be enrolled in both Part A and B to enroll in an MA plan. You will continue to pay for Part B while you are enrolled in a Medicare Advantage plan.

Medicare Advantage

Private plans that pay instead of Medicare

Medicare Advantage plans are cheaper than Medigap plans because instead of you seeing any Medicare provider, Medicare Advantage (MA) plans limit your choices to doctors that contract with them and deliver your care through the MA plan’s network.

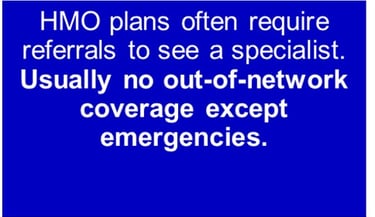

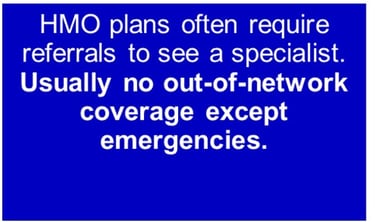

Most plans offer either an HMO or PPO network

HMO plans are more restrictive, often requiring you to choose a primary care physician (PCP) and see that doctor first for a referral before you can see a specialist. Many HMO plans don’t offer out of network coverage except in an emergency.

Preferred Provider Organization plans are more flexible, allowing you to see any doctor who is willing to accept and bill the plan. Treatment outside of the network will come at higher costs to you though.

Many MA plans include a built-in Part D drug plan, as we mentioned, and they can also include some extras like routine vision benefits, preventive dental care and even gym memberships. These benefits do tend to be somewhat limited but they appeal to many beneficiaries.

Keep in mind that insurance companies are in business to make money. They may require a doctor to submit requests for prior authorizations more often than you would experience under Original Medicare.

MA premiums are lower up front but that’s because you pay more as you go.

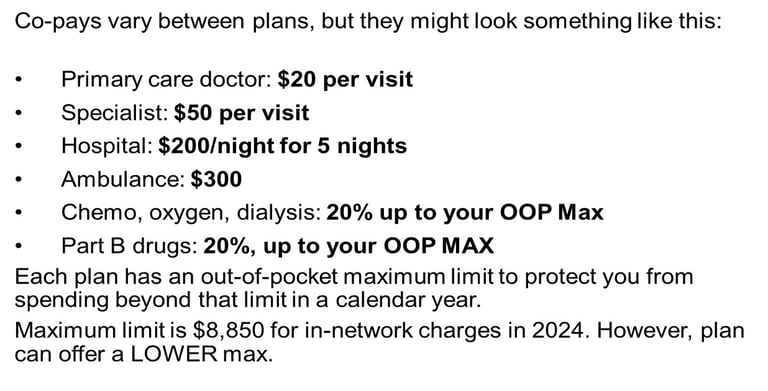

Medicare Advantage

What the co-pays may look like

Each Medicare Advantage plan sets its own premiums and co-pays for various services. This will vary by plan. This is just one example of what you might spend on a plan. Note that many Medicare Advantage plans will charge you up to 20% for expensive items such as cancer treatments and dialysis. You’ll pay the out-of-pocket co-pays and coinsurance each year up until you reach the plan’s stated Maximum out-of-pocket (MOOP) limit for the year. Each plan determines where to set the MOOP but the maximum limit can not be any higher than $9250 for 2026.

This is a significant difference from Medicare Part B which has no out-of-pocket maximum

Common question

Are Medicare Advantage plans bad?

Each fall you’ll probably have your favorite show interrupted multiple times with some celebrity encouraging you to buy a Medicare Advantage plan

These “zero dollar” plans seem too good to be true.

This leaves many asking, “Are Medicare Advantage plans bad?”

Not necessarily, they are different- sometimes a great fit, sometimes not.

The top advantage is price. The monthly premiums are often lower than Medicare Supplement/Medigap plans. The top disadvantage is that not all hospitals and doctors accept Medicare Advantage plans.

Though, there is no debate when in comes to which plan is more comprehensive. Medigap plans have fuller coverage all the way around but typically cost more.

Medicare Advantage

The unexpected costs

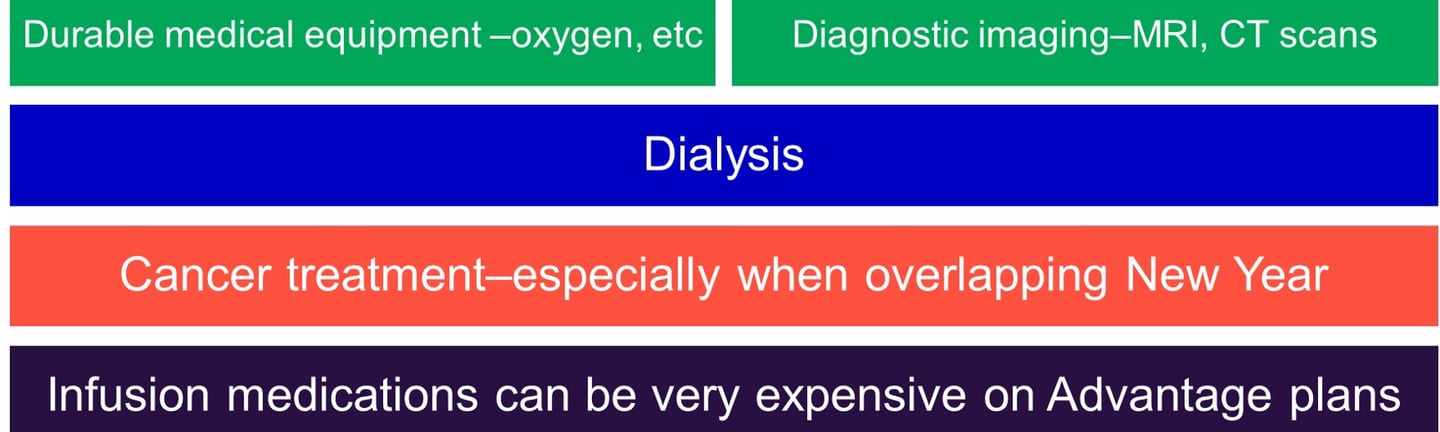

You may pay up to 20% for these items on many plans.

While each plan is different, you should carefully review the plan’s Summary of Benefits before enrolling. Some of the things that could cost as much as 20% on Medicare Advantage plans are durable medical equipment, diagnostic imaging, cancer treatment, dialysis, and Part B drugs administered in a doctor’s office. Be aware of these as they can be costly in a future year if you incur health conditions requiring any of this equipment or treatment

Medicare Advantage

The things too many beneficiaries don’t realize

Every September, your Medicare Advantage plan will send you an Annual Notice of Change document. Review it carefully to see what is being changed inside your plan for next year. Is the premium increasing? Did the carrier drop any of your important medications from the formula for next year? If so, you may want to switch plans

You can also return to Original Medicare during the Fall AEP, but if you wish to get a Medigap plan to go alongside Medicare, remember that you’ll have to answer health questions in most states to get this coverage. There is no guarantee once your one-time six-month open enrollment period has passed unless you live in a state that offers guaranteed enrollment

Common Medicare Mistakes

Medicare misstep #1

Confusing the Medigap OEP with the Fall AEP

Medicare mistake

The most common

Not understanding the difference - The two Medicare routes are NOT alike

Arguably the worst Medicare mistake one can make, with the greatest consequences– not understanding the difference between Original Medicare with a Medigap and Part D Plan and a Medicare Advantage plan.

Do your research carefully and make sure you understand how the different plans work.

Another Medicare Mistake - Enrolling too late

Not enrolling at the right time

There are many people who are unaware that Medicare is primary when you have small employer coverage or retiree coverage. They miss their Initial Enrollment Period and get hit with late penalties later on.

Also, if you have an individual health plan through the ACA, you should enroll in Medicare at age 65. ACA plans were never intended to replace Medicare and if you fail to enroll in Medicare at 65, you will incur penalties later on. Leave the ACA plan and go on Medicare.

Employer coverage

You plan on working past age 65-

What to take into account

The size of your company matters

The key thing to keep in mind is that the size of your company matters.

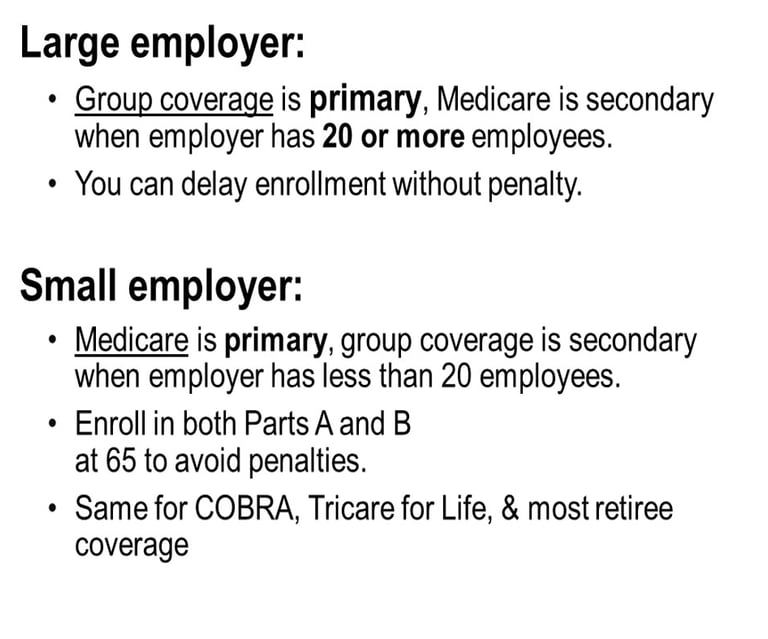

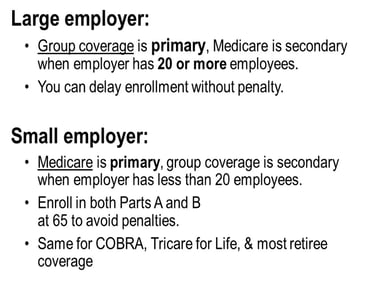

Recommendation for large employer:

If your company has 20 or more employees your group coverage is primary and Medicare is secondary.

Enroll in just Part A, delay Parts B and D.

No penalty for doing so when you work for a large employer

Caveat: don’t enroll in any part of Medicare if contributing to an HSA

Later when you retire, you’ll submit Form CMS-40B–an application for Part B–to SS along with Form CMS-L564, which your employer fills out verifying your employment and employer health coverage since the time your turned 65

Recommendation for small employer:

If your company has less than 20 employees, your Medicare coverage is primary and your group coverage is secondary.

Enroll in both Parts A and B during your IEP

Otherwise, you may pay for all your own outpatient coverage and incur a 10% penalty

Potential for 10% cumulative late penalty.

You can delay enrollment into Part D without penalty if employer drug coverage is creditable. (Keep your creditable coverage letter that your employer insurance company sends you.)

You must discontinue contributing into any HSA

The best thing to do when working past 65 is to start planning early by talking to your employee benefits representative.

For questions or to receive a quote, email us at medicare@ healthwealth360365.com (or click the button below)

HSA Participants - Important Actions Required

The "6-month rule" is a Medicare regulation that can trigger tax penalties for Health Savings Account (HSA) owners who delay Medicare enrollment past age 65. When you eventually enroll, Medicare Part A coverage is often backdated by up to six months, which retroactively disqualifies you from making HSA contributions during that period.

How the Rule Works

Retroactive Coverage: If you apply for Medicare Part A after you turn 65, your coverage is automatically backdated up to six months (but never earlier than your 65th birthday month).

HSA Ineligibility: IRS rules state you cannot contribute to an HSA if you are enrolled in any part of Medicare. The retroactive coverage period counts as being enrolled, making any contributions during those months "excess contributions".

Penalties: Contributions made during the retroactive period are subject to a 6% excise tax for every year the excess funds remain in the account

When the Rule Applies

Scenario Does the 6-Month Rule Apply?

Enrolling at exactly 65 No. Coverage starts the first day of your birth month; there is no look-back before age 65. |

Enrolling after 65 Yes. Part A is backdated up to six months from your application date. |

Collecting Social Security Yes. Enrolling in Social Security at 65 or older triggers automatic Part A enrollment with the same 6-month look-back. |

How to Avoid Penalties

Stop Contributions Early: It is a best practice to stop all HSA contributions (including employer matches) at least six months before you plan to apply for Medicare or Social Security.

Prorate Your Limit: If you enroll mid-year, you must calculate your annual contribution limit by dividing the yearly maximum by 12 and multiplying by the number of months you were eligible before your retroactive Medicare start date.

Correct Mistakes: If you accidentally contribute during the retroactive period, you can avoid the 6% penalty by withdrawing the excess funds and any associated earnings before your tax filing deadline (usually April 15).

Connect

Insurance services provided through Wealthstream Financial Solutions, Inc

Wealth Management services provided through RCM Wealth Advisors

Alternative Investments provided through RCM Alternatives

Private Placements provided through Wealthstream Financial Solutions, Inc

Services

contact@healthwealth360365.com

© 2025. All rights reserved.