Annuities

An annuity is a long-term insurance contract that provides a stream of guaranteed income, often used to supplement retirement savings. You pay premiums, either in a lump sum or over time, and in return, the insurance company agrees to pay you regular disbursements for a set period or for the rest of your life.

How annuities work

Annuities generally operate in two distinct phases:

Accumulation phase: During this period, you make payments into the annuity, and the money grows on a tax-deferred basis. The value of your annuity depends on the type of annuity you choose.

Payout (or annuitization) phase: You begin to receive payments from the annuity. This can happen in one of two ways:

Annuitization: You convert the contract's value into a stream of guaranteed, regular payments for a specific period or for life.

Withdrawals: You take a lump sum or a series of withdrawals from the accumulated value.

Common types of annuities

Annuities can be categorized based on when payments begin (immediate vs. deferred) and how the money grows (fixed, variable, or indexed).

Based on timing of payments:

Immediate annuity: With an immediate annuity, you make a single, lump-sum payment and begin receiving income almost right away, typically within a year. This is best suited for people who are retired or nearing retirement and want to convert a portion of their savings into a predictable, immediate income stream.

Deferred annuity: This type of annuity is designed for longer-term savings, with payments beginning at a future date you choose. This allows your money to grow tax-deferred during the accumulation phase, potentially resulting in larger payouts later.

Based on investment growth:

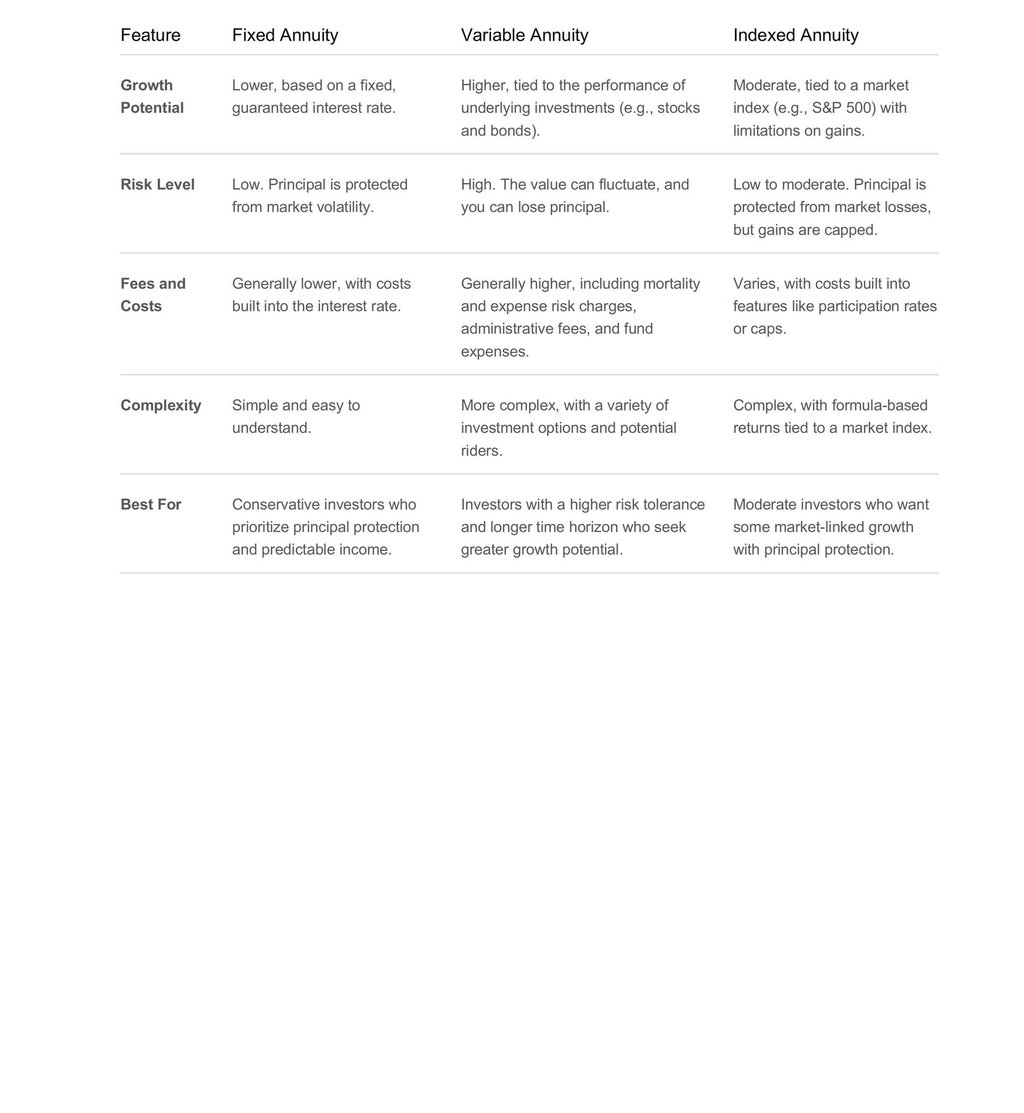

Fixed annuity: A fixed annuity offers a guaranteed, fixed rate of return for a set period during the accumulation phase. It is a lower-risk option because your principal is protected from market volatility. During the payout phase, you receive a guaranteed, predictable stream of income.

Variable annuity: This type of annuity invests your premiums in various investment subaccounts, similar to mutual funds. The value of your annuity and your future payments can fluctuate based on the performance of these investments, offering the potential for higher returns but also carrying higher risk, including the possibility of losing principal.

Indexed annuity: An indexed annuity is a hybrid product that offers a blend of safety and growth potential. It provides a guaranteed minimum return, and additional returns are linked to the performance of a market index, like the S&P 500. However, your potential gains are often limited by a "cap," "participation rate," or "spread".

Annuity Comparison Chart

Who should consider an annuity?

An annuity can be a valuable tool, but it's not the right fit for everyone. It's often best for individuals who have already maxed out other retirement accounts and want a predictable income stream to cover essential expenses in retirement. Those with a lower risk tolerance who prioritize guaranteed income over potentially higher, but more volatile, investment returns may also find an annuity appealing.

The Pro's and Con's

Pros of annuities

Guaranteed income for life: Many annuities are structured to provide guaranteed payments for as long as you live. This feature, which is particularly useful for combating the risk of outliving your savings, makes annuities a reliable "personal pension".

Tax-deferred growth: Your money grows on a tax-deferred basis, meaning you don't pay taxes on the interest, dividends, or capital gains until you start making withdrawals. This allows your savings to compound faster over time.

No annual contribution limits: Unlike 401(k)s and IRAs, nonqualified annuities have no annual IRS contribution limits. This makes them an option for those who have already maxed out other retirement accounts.

Principal protection: Certain types, such as fixed and indexed annuities, offer a level of principal protection, ensuring your initial investment is not lost due to market downturns.

Estate planning benefits: Annuities can be customized with features that can help with estate planning by allowing you to designate a beneficiary to receive payments after your death.

Customizable features: You can customize your contract with riders to include additional benefits like guaranteed lifetime withdrawals, cost-of-living adjustments, or higher payouts for long-term care.

Cons of annuities

High fees and commissions: Many annuities, especially variable ones, come with substantial costs that can eat into your returns. These include administrative fees, mortality and expense risk charges, and commissions paid to the agent who sold the product.

Limited liquidity: Most annuities are long-term investments, and funds are locked up for a surrender period, often seven to ten years. Taking early withdrawals can trigger high surrender charges from the insurance company.

Early withdrawal penalties: The IRS typically imposes a 10% penalty on the taxable portion of withdrawals made before age 59½, in addition to ordinary income tax.

Complexity: Annuity contracts can be difficult to understand due to complex features, fee structures, and payout options. This can make it challenging for the average person to know what they are actually paying for.

Inflation risk: For fixed annuities, the purchasing power of your income can be eroded by inflation over time. While some contracts offer inflation protection, it often comes at an extra cost or results in a lower initial payout.

Taxes on gains at ordinary income rates: While growth is tax-deferred, when you do take distributions from a nonqualified annuity, the earnings are taxed as ordinary income, which may be higher than the capital gains tax rates on other investments.

Risk of insurer default: Annuity guarantees are only as strong as the financial health of the issuing insurance company. While state guaranty associations provide some protection, it is important to choose a financially stable insurer.

For questions or to receive a quote, email us at annuity@healthwealth360365.com (or click the button below)

Connect

Insurance services provided through Wealthstream Financial Solutions, Inc

Wealth Management services provided through RCM Wealth Advisors

Alternative Investments provided through RCM Alternatives

Private Placements provided through Wealthstream Financial Solutions, Inc

Services

contact@healthwealth360365.com

© 2025. All rights reserved.